Credit is a fundamental aspect of financial health, influencing everything from loan approvals to rental agreements. Understanding the differences between credit reports and credit scores, and knowing how to manage and protect your credit, is crucial for maintaining financial stability. This guide explores essential topics such as the nature of credit reports and scores, the frequency of report updates, factors affecting credit scores, and strategies for credit repair and building. It also addresses how personal and business credit differ and provides steps to handle identity theft effectively.

Understanding Credit Reports & Scores

Understanding how important your credit is can make a big difference. It plays a pivotal role in financial health, determining your access to loans, mortgages, and rental agreements. One of the key benefits of having a good credit score is access to better interest rates and terms, whereas poor credit may result in higher costs and obstacles to getting credit. Good credit is essential for financial stability and opportunities, making it important to manage credit responsibly and monitor one’s credit report regularly to ensure accuracy and address any issues promptly.

Credit Report vs. Credit Score

What are credit reporting agencies? They’re companies like Experian, Equifax, and TransUnion that compile credit reports based on your financial history. These bureaus gather information from various sources, including banks, credit card companies, and lenders, which report your credit account details, payment history, and other relevant financial data.

In contrast, a credit score is a numerical representation of this credit history, calculated based on the information in the credit report. The score is used by lenders to evaluate creditworthiness and make lending decisions. Essentially, while the credit report provides a comprehensive overview of one’s credit behavior, the credit score offers a quick, quantifiable measure of credit risk. You can learn more in Credit Scores and Credit Reports: What’s the Difference?

How Often Does My Report Update?

Wondering how often credit reports update? They’re generally updated on a monthly basis as creditors and lenders provide fresh data to the credit bureaus. However, the exact timing can vary depending on when creditors submit their updates and when the credit bureau processes them. While major changes might reflect quickly, there can be a lag between when an event occurs and when it appears on a credit report. Regularly checking one’s credit report is advised to ensure accuracy and to stay informed about one’s credit status.

What Impacts My Score?

What actually hurts my credit score? Factors such as late payments, high credit utilization, and too many inquiries can all have a negative effect. Key issues include late payments, which can significantly damage credit, and high credit card balances relative to credit limits, which increases credit utilization. Other detrimental factors include having accounts sent to collections, applying for multiple new credit accounts in a short period (which can suggest financial distress), and maintaining a high number of credit inquiries. Additionally, closing old accounts can reduce the average age of credit history, further affecting the score. New to credit scores? Learn how to read your score here. Wondering what your beginning score is or how high your score can go? Check out these articles; ‘What Credit Score Do You Start With?’ and ‘What Is The Highest Credit Score You Can Have?’

Different Scoring Models

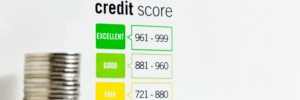

Have you ever wondered how your credit score measures up? Credit scoring models vary in how they assess creditworthiness, with FICO and VantageScore being the most prominent. Each scoring model also has different ranges that they consider good or bad.

- FICO Score: Developed by Fair Isaac Corporation, it is widely used by lenders and has multiple versions. Key models include:

-

- FICO 8: A recent model that assesses credit risk with a focus on recent credit behavior and allows for some flexibility regarding high credit utilization.

- FICO 5: An older model used primarily for mortgage lending, which may weigh credit factors differently and emphasize long-term credit history.

To learn more about these two common FICO Scores, check out ‘FICO 5 vs FICO 8: Understanding Credit Scores.’

- VantageScore: Created by the three major credit bureaus (Experian, Equifax, TransUnion), it provides a consistent scoring approach across all three bureaus. It also uses a scale from 300 to 850 and considers similar factors to FICO, such as payment history and credit utilization, but with some variations in weight and criteria.

Each model has its nuances, and lenders may use different versions depending on their specific needs and the type of credit being applied for. For more information on VantageScore, explore ‘What is VantageScore?’

Credit monitoring vs Credit building vs Credit repair: What’s the difference?

Credit monitoring tracks your credit report and score for changes or issues, providing alerts for potential fraud or significant updates. If you’ve ever asked yourself ‘why did my credit score drop for no reason?’ regularly monitoring your credit can help you spot and address unexpected drops. Find out more about what items you should regularly review on your credit report and why you should check your credit reports here.

Credit building involves actions to improve your credit history and score, like using credit responsibly and maintaining low credit utilization.

Credit repair focuses on correcting errors or negative items on your credit report to improve your score and ensure accurate information.

Repair or Build – What Should I do?

To determine if you need to repair or build your credit, assess your credit report and score. If you find numerous errors, negative items, or significant issues affecting your score, you may need credit repair to correct inaccuracies and address negative entries. On the other hand, if your credit history is sparse or you lack a solid credit foundation, learning how to start building credit with no credit and how to build positive credit habits can be crucial to establishing and improving your credit profile. Reviewing your credit report regularly can help you identify which approach is appropriate based on your specific credit situation.

Credit Repair

How does a mistake on my credit report hurt me? Errors can severely damage your credit score, affecting your ability to secure loans and favorable terms.They might lead to higher interest rates, loan denials, or even affect employment opportunities. If you’re looking for guidance on how to dispute an error on your credit report, begin by obtaining reports from each of the major credit bureaus, then carefully identify inaccuracies and gather supporting documents. Identify the inaccuracies and gather supporting documents. Then, file a dispute with the credit bureau, detailing the error and providing evidence.

How credit repair affects your credit can be significant, as it works to improve your score by addressing inaccuracies and removing negative entries from your credit report. The time needed for credit repair can vary based on the extent of the issues and the steps involved. Minor errors might be corrected within a few months, while more significant issues like severe delinquencies or bankruptcies can take several years to resolve.

You can always hire a company for credit repair, but before you do, it’s wise to compare different services. Evaluate their reputation, transparency, and how much their credit repair costs to find the best fit for your needs. Look for companies with positive reviews, clear pricing, and a history of successful credit repair. There are many ways to repair your credit for free. Discover how to repair credit for free and find out what credit repair service is right for you.

Credit (Re)Building

Building credit is important because it significantly impacts your financial opportunities and stability. You should start building credit as early as possible, even in your late teens or early twenties.

If you’re wondering what is the fastest way to rebuild bad credit, here are some tips:

- Ensure timely payments on all accounts

- Keep credit utilization below 30% of your limit

- Maintain a long credit history by keeping old accounts open

- Aim for a mix of credit types, such as credit cards and installment loans

- Limit hard inquiries

- Consider obtaining a secured credit card or a credit-builder loan

How long does it take to improve your credit score? Well, the process can span from several months to a few years, depending on your starting point and actions. You might see minor improvements within 3 to 6 months with steady, responsible credit use and timely payments.

Personal and Business Credit: What You Need to Know

Personal and business credit serve different purposes and are managed separately. Personal credit reflects an individual’s financial behavior and affects personal loans, credit cards, and financial opportunities.

In contrast, business credit evaluates a company’s financial health and impacts its ability to secure business loans and credit.

Personal credit can influence business lending. If you’re wondering, ‘can your personal credit affect your small business?‘ the answer is yes, especially for startups or small businesses with limited credit history.

How to Improve Your Business Credit Score

If you want to know how to improve your business credit score, start by establishing a strong credit profile with major credit bureaus. Use separate bank accounts and credit cards for business transactions to maintain clear financial boundaries. Make all payments on time, including loans and vendor invoices, to build a positive payment history. Keep credit card balances low relative to your limits and avoid maxing out your credit. Cultivate good relationships with suppliers for positive trade references and regularly monitor your credit reports to identify and correct any errors. Additionally, consider requesting higher credit limits to improve your credit utilization ratio and enhance your business credit score.

Understanding and Addressing Identity Theft

Identity theft involves someone using your personal information, like Social Security numbers or credit card details, without permission to commit fraud. This misuse can lead to unauthorized transactions, loans, and significant financial damage.

How to Fix Your Credit After Identity Theft

- Report the Theft: File a report with the FTC and your local police to document the crime.

- Place a Fraud Alert: Contact a credit bureau to add a fraud alert to your credit report.

- Review Your Credit Reports: Check for unauthorized accounts and dispute inaccuracies with credit bureaus.

- Close Fraudulent Accounts: Notify financial institutions to close any fraudulent accounts.

- Update Your Information: Change passwords and secure your accounts.

- Monitor Your Credit: Regularly check your credit reports for any new fraudulent activity.

These steps will help you repair your credit and address the damage caused by identity theft. For a more detailed guide, click here.

Conclusion

Maintaining a strong credit profile requires ongoing attention and proactive management. By understanding how credit reports and scores work, staying updated on your credit status, and knowing how to improve or repair your credit, you can safeguard your financial health. Whether you need to build your credit from scratch, fix errors from identity theft, or improve your business credit, taking these steps will help you achieve better financial opportunities and stability. Regular monitoring and responsible credit practices are key to a successful financial future.

Frequently Asked Questions

Is Dovly Free Credit Repair?

How is Dovly different?

Can I trust Dovly?

How many points can I expect my score to go up?

COMPANY

SUPPORT

LEGAL

CREDIT HELP

COMPARE OPTIONS

© 2026 Dovly, Inc. All rights reserved.