What Credit Score is Needed to Buy a Car?

Before you hit the road in that dream car, there’s one crucial checkpoint you can’t ignore—your credit score. Whether you’re buying a new ride or a reliable used car, your credit score can either help you drive off the lot or keep you browsing. This guide will break down everything you need to know about credit scores for car purchases, from understanding the key factors that affect your score to how lenders evaluate your overall financial picture. Ready to take control of your car-buying journey? Let’s get started!

Imagine finally deciding on your dream car only to be told your score doesn’t make the cut. Credit scores are the financial passports we seldom consider until a big purchase surfaces. Understanding this silent gatekeeper can determine whether you’ll drive off the lot in style or continue to window shop.

This article will steer you through the essentials of scores needed to buy a car, unpack the weight your score carries, delve into other pivotal factors considered by lenders, and finally, shift gears to help you prepare for a smooth purchase. Get ready to embark on the road to understanding scores and securing that new set of wheels.

What is a Credit Score?

A credit score is a crucial financial metric that represents an individual’s creditworthiness. Generated using information from credit reports, the average credit score range is between 300 and 850. Lenders, including auto lenders, rely on scores to gauge the risk of extending a loan, determining loan approvals, and setting interest rates.

Key factors influencing scores include:

- Payment History: This is the most significant factor impacting a score. Lenders want to see a history of on-time payments with no missed or late payments. If you consistently pay your bills promptly, it shows that you are a responsible borrower.

- Credit Utilization Ratio: This ratio measures how much of your available credit you are currently using. Lenders prefer to see a lower percentage, as it indicates that you are not overly reliant on credit. It is recommended to keep your credit utilization ratio below 30%. For example, if your total credit limit across all your cards is $10,000, try to keep your balances below $3,000.

- Length of Credit: This factor considers the length of time you have had credit accounts. Longer credit histories are generally viewed as more positive, as they provide a more extensive track record for lenders to assess your creditworthiness. If you are new to credit, it may be harder to get approved for a car loan, but it is not impossible.

- Types of Credit: Having a good credit mix, such as credit cards, student loans, and auto loans, can positively impact your score. It demonstrates your ability to manage different forms of credit

- New Credit: Opening multiple new credit accounts within a short period can negatively impact your score. It may be seen as a sign of financial instability or desperation for credit. When buying a car, it’s important to avoid opening new credit accounts right before or during the car shopping process.

Credit bureaus utilize data from credit accounts and loans to calculate these scores. Higher scores indicate lower risks for lenders, potentially translating into better loan terms. Hence, regularly reviewing credit reports from major credit bureaus and maintaining healthy financial habits, like making time payments and minimizing credit utilization, are vital for achieving and sustaining a favorable score.

Credit Score Impact

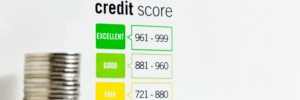

When considering the purchase of a car, your score plays a pivotal role. Lenders scrutinize your financial history to determine whether you’re eligible for loans and to set the terms, such as your monthly payment or interest rate. Generally, a higher score can lead to better loan terms. While there’s no uniform minimum credit score required to buy a car, scores are typically segmented as follows:

- Excellent Credit: 781-850

- Good Credit: 661-780

- Fair Credit: 601-660

- Poor Credit: 501-600

- Bad Credit: 300-500

Even with poor credit or bad credit, you could still secure financing, but potentially at the cost of thousands of dollars more due to higher interest rates. Responsible financial behavior over time, including paying bills on time and wisely managing loan payments, will help improve your credit and increase your chances with potential lenders.

Other Factors Considered by Lenders

A credit score is a numerical expression based on a level analysis of a person’s credit files – it dictates your creditworthiness to lenders. As one of the crucial elements in auto financing, your score can greatly influence the terms of your loan, including interest rates and repayment periods. But it’s not the only player in the game.

Debt-to-Income Ratio

This metric is a crucial element in the auto lending decision process. Your debt-to-income ratio (DTI) measures how much of your gross monthly income is used for paying debts. The lower your DTI, the more favorably lenders may view your loan application. A DTI of 40% or lower is commonly preferred by lenders, signaling that you have a manageable level of debt relative to your income. You can find out more about your debt-to-income ratio here.

Employment History

Lenders typically favor applicants with a steady employment history, as it indicates a reliable source of income for making regular loan payments. Longevity in your current job or a consistent work history within the same industry can reassure lenders of your financial stability. Frequent job changes or periods of unemployment could raise concerns about your ability to maintain consistent loan payments.

Down Payment

The amount of money you are able to put down on a vehicle can significantly affect your loan terms. A larger down payment often translates into smaller monthly payments and could possibly result in lower interest rates. While there are options available for little to no down payment, offering a substantial down payment reduces the lender’s risk and thus could bolster your chances of loan approval.

By considering these additional factors alongside your score, lenders create a comprehensive financial profile to assess risk and determine the most suitable loan conditions for you.

Preparing to Buy a Car

Purchasing a vehicle is a significant financial decision that demands careful consideration and preparation. To ensure a smooth car-buying process, it’s vital to assess your credit. However, your score is not a standalone metric; understanding other financial components and the nuances of auto financing is equally important. Equip yourself with knowledge about the costs involved, the effect of your credit history, and the importance of a good score for securing favorable loan conditions.

Research

Embarking on your car-buying journey begins with diligent research. Start by determining the type of vehicle that suits your needs and budget. Consider the trade-offs between new and used cars, including depreciation, maintenance costs, warranties, and overall value. Explore various lenders, such as banks, credit unions, and online financial institutions, to understand the different financing options and average interest rates. Be sure to check for any hidden fees. Additionally, familiarize yourself with the latest car models, consumer reviews, safety ratings, and the average price of the cars you are interested in. It may be beneficial to contact your insurance company to identify any insurance costs associated with the car you are considering purchasing.

Review Your Finances

A thorough analysis of your personal finances is crucial before committing to a vehicle loan. Begin by establishing a realistic budget that includes the potential payment for the car loan each month, insurance, fuel, maintenance, and any additional costs related to vehicle ownership. Calculate your debt-to-income ratio to confirm that you can comfortably afford the new expense without overextending your financial obligations. Evaluate your savings to determine the amount you can allocate for a down payment, as a larger down payment may lead to more favorable loan terms and lower interest rates. Based on your financial situation, leasing a car may be more affordable than purchasing a car.

Get Your Credit In Order

Your credit is a pivotal element in obtaining a car loan. Acquire copies of your credit reports from the major credit bureaus; Experian, Equifax and TransUnion to ensure accuracy and to dispute any discrepancies that may harm your score. Aim to pay down credit card balances and avoid taking on new debt, as both actions can improve your credit utilization ratio—a key factor in credit scoring models. Establish a pattern of making all payments on time, including any existing loans or bills, to strengthen your payment history. If your credit is less than ideal, consider waiting and working on your credit before applying for auto loans to potentially secure better rates and save thousands of dollars over the life of the loan.

Conclusion

In conclusion, your credit plays a significant role in determining whether you can buy a car and the terms of your loan. While there is no specific minimum score required to buy a car, having a higher score will generally lead to better interest rates and loan options.

It is vital to keep your credit in good shape by making timely payments, keeping card balances low, and avoiding new credit applications before buying a car. Additionally, it’s important to consider other factors that lenders will evaluate, such as your income, employment history, and down payment.

So, whether you’re dreaming of a shiny new vehicle or a reliable used car, take the time to build and maintain a healthy credit profile. Your future self will thank you when you’re cruising down the road in your new set of wheels.

By methodically preparing for your car purchase, reviewing your finances, and optimizing your credit, you position yourself as a well-qualified buyer, ready to negotiate the best possible terms for your loan. Enroll with Dovly AI today for free to see where your credit is currently at.