Kikoff vs. Kovo: Which Credit Builder Is Better for You?

If you’re comparing Kikoff vs Kovo, you’re likely trying to figure out which is the best credit-building app that will actually help you build credit — and whether the cost is worth it. The short answer: Kikoff adds a revolving credit line to your credit report, while Kovo reports installment-style monthly payments. Many people comparing these tools are focused on simple credit building strategies that help them build credit without taking on high-interest debt and reporting to the credit bureaus.

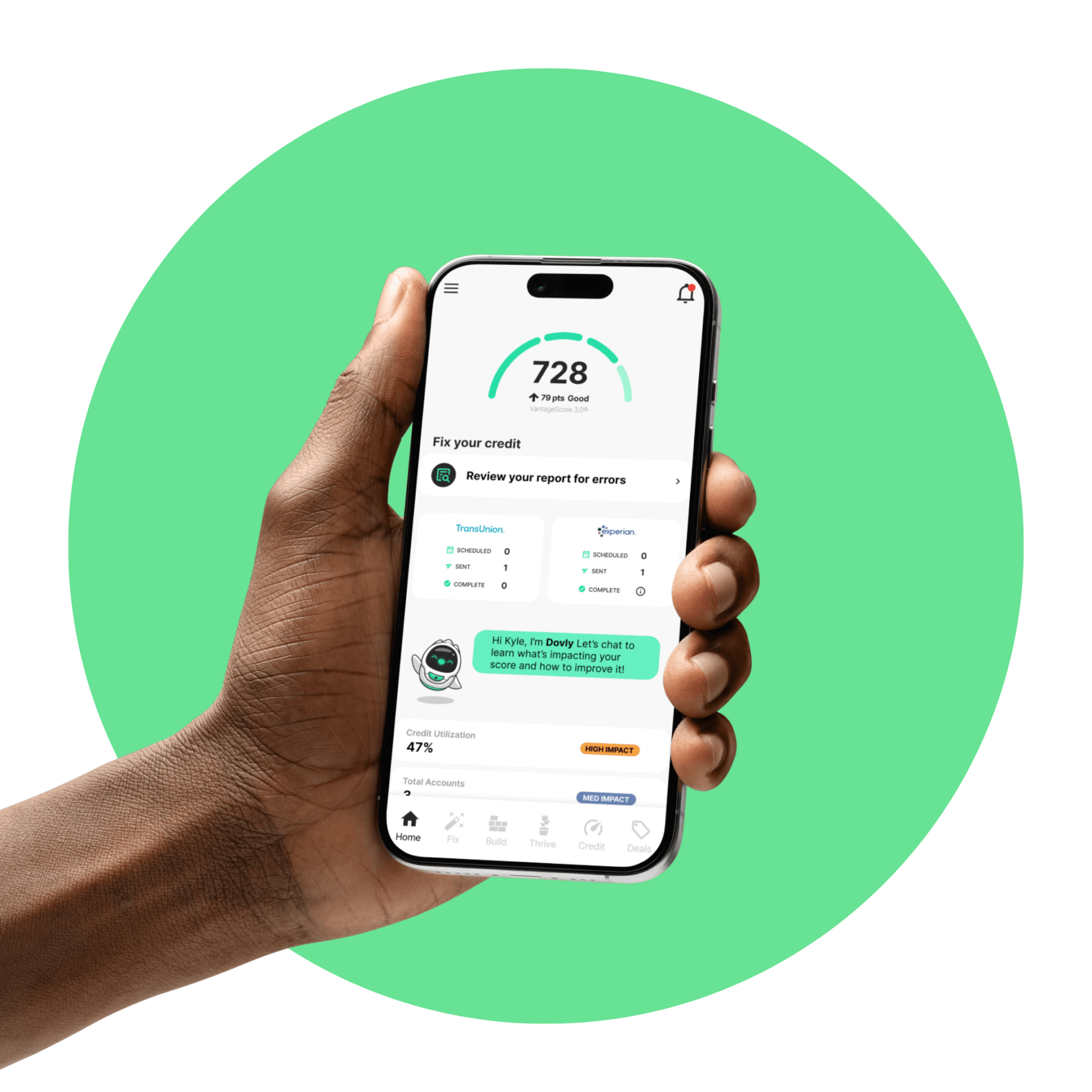

Dovly AI is an all-in-one credit platform designed to build, fix, and protect your credit simultaneously. Unlike basic credit building apps, it provides a $2,000 tradeline (Dovly Build) reported to Experian and comprehensive rent reporting (Dovly Rent & Bills) that can add up to 24 months of past and ongoing utility history to TransUnion. This “dual-build” strategy is integrated with an AI engine that automatically identifies and disputes inaccurate negative items to optimize your score from every angle.

What You Can Achieve with Dovly AI

Get approved for credit cards

No more denials based on outdated information.

Plan for major life milestones

Don’t let credit hold you back.

Buy a house or apartment

Lenders value a strong, stable credit score.

Save thousands on interest

A better score means better rates.

Purchase a car

Secure lower interest rates and better loan terms.

Achieve financial independence

Take control of your credit and your future.

– Paisley G.

I absolutely love this app. It does everything. I am so happy to be living in the age of AI

– Brett B.

– Hannah T.

✅ Start Free with Dovly AI Today

No calls. No paperwork.No commitment.

Just your score—going up.

COMPANY

SUPPORT

LEGAL

CREDIT HELP

COMPARE OPTIONS

© 2026 Dovly, Inc. All rights reserved.