How to Improve Experian Credit Score

Your credit score is a snapshot of your financial health—and improving it is totally within reach. This guide covers the basics: what affects your score, why it might differ across credit bureaus, and practical tips to boost it. From paying on time to lowering utilization and keeping old accounts open, these small moves can make a big impact. Plus, learn how Dovly’s AI-powered tools can help you dispute errors and monitor your progress with ease.

Your credit score is like your financial report card—it tells lenders how well you manage credit. If your credit score isn’t where you want it to be, don’t stress! Improving it is totally doable with the right steps.

In this guide, we’ll break down how credit scores work, what affects them, and what you can do to boost yours. Let’s get started!

How to Improve Your Credit Score

First, let’s talk about practical steps you can take to raise your credit score.

1. Make On Time Payments

Late payments are one of the biggest credit score killers. If you’re someone who struggles with remembering due dates, automate your payments or set monthly reminders.

2. Reduce Your Utilization

Using too much of your available credit can drag down a good credit score. Try to keep your utilization below 30%—or even better, under 10%. Instead of juggling balances, focus on paying off cards with the highest balances to reduce your utilization.

3. Check Your Credit Report for Errors

Mistakes happen! If you see errors on your credit report, dispute them. You can easily access a free copy of your credit report from each bureau once a year at AnnualCreditReport.com.

4. Keep Old Credit Accounts Open

The length of your credit history matters. Even if you don’t use an old card often, keeping it open can help maintain your score. Closing old accounts can shorten your credit history, which can negatively impact your score.

5. Diversify Your Credit Mix

Having a mix of different types of credit—like a credit card and an installment loan—can help improve your credit history. If you only have credit cards, consider adding an installment loan like an auto loan or a personal loan.

What Is an Experian Score?

Experian is one of the three major credit bureaus, along with Equifax and TransUnion. It gathers data from lenders and other sources to generate a credit score that helps lenders assess your creditworthiness.

Experian does not have its own unique scoring formula for your Experian credit file; instead, it provides credit scores based on widely used scoring models like FICO® Score and VantageScore®. Lenders using Experian credit reports may rely on different versions of these models depending on their needs.

While Experian also offers its own credit monitoring services and Experian Boost (which can add certain payments to your credit report), the credit scores themselves are still calculated using standard industry models.

Why Your Score May Vary Across the Three Bureaus

It’s important to note that your credit score may vary slightly between each credit bureau (Experian, TransUnion, and Equifax), even if the same scoring model (like FICO) is used. This can happen for several reasons:

Data Reporting Differences

Not all lenders report to every credit bureau. For example, one lender may report on your Experian credit report but not on your TransUnion credit report. This means each bureau might have slightly different information on your credit report, which could lead to differences in your credit scores.

Different Scoring Models

Each credit bureau may use different scoring models. While FICO is the most widely used model, there are variations (e.g., FICO 8 vs. FICO 9), and some lenders may use different versions or even VantageScore.

Timing of Data Updates

Each bureau updates its credit reports at different times. As a result, one credit report might have more recent data than another, impacting your score.

How Is a Credit Score Calculated?

Your credit score is calculated using a variety of factors, each weighted differently. Let’s dive deeper into the key elements that make up your credit score:

1. Payment History (35%)

Your payment history is the most significant factor affecting your credit score. It reflects whether you’ve paid your bills on time or missed payments in the past. A consistent record of on-time payments shows lenders you’re reliable and trustworthy, which boosts your credit score.

2. Credit Utilization (30%)

Credit utilization refers to the ratio of your current credit card balances to your credit limits. It shows how much of your available credit you’re using, which is a strong indicator of how risky you might be to lenders.

3. Length of Credit History (15%)

The length of time you’ve been using credit can impact your score. Generally, a longer credit history is seen as more favorable because it shows your ability to manage credit responsibly over time.

4. Credit Mix (10%)

Your credit mix refers to the various types of credit accounts you have, including credit cards, installment loans, mortgages, and auto loans. A variety of credit types indicates you’re capable of managing different kinds of debt responsibly.

5. New Credit Inquiries (10%)

When you apply for new credit, the lender will conduct a hard inquiry (also called a hard pull) on your credit report. Multiple hard inquiries within a short time frame can signal to lenders that you’re taking on too much debt, which could lower your score.

These five factors work together to form your overall credit score. While each is important, payment history and credit utilization tend to have the greatest influence, so focusing on these areas can have the most significant impact when trying to improve your score.

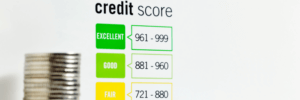

Credit Score Ranges: What They Mean

Your credit score falls within a certain range that determines your creditworthiness. Understanding where your score falls is key to knowing how lenders will view you. Here’s a detailed breakdown of the different score ranges and what they mean for your financial options:

300-579: Poor

A score in this range indicates poor credit health, which means you’re considered a high-risk borrower. It may be difficult to get approved for credit cards, loans, or even a rental lease, and if you’re approved, the terms will likely be very unfavorable.

- What it means:

- You might face higher interest rates and lower loan limits, even if you are approved for a loan.

- You may need to look into secured credit cards or credit-builder loans to improve your credit score.

580-669: Fair

With a fair credit score, you’re in a better position than those with poor credit, but lenders still view you as a somewhat risky borrower. You might qualify for certain types of credit, but your interest rates will likely be higher than those with good credit.

- What it means:

- You’re likely to get approved for a loan or credit card, but you may face higher interest rates.

- You might still struggle to secure a mortgage or car loan with competitive rates.

670-739: Good

A score in the “good” range means you’ve demonstrated responsible credit behavior, and lenders are generally confident in your ability to manage debt. You’ll likely qualify for credit with better terms, such as lower interest rates and higher credit limits.

- What it means:

- You’ll qualify for most credit products, including personal loans, mortgages, and credit cards with decent interest rates.

- You’re likely to receive more favorable terms on loans and credit lines.

740-799: Very Good

If your credit score falls within the “very good” range, you’re considered a low-risk borrower. Lenders trust that you’re responsible with credit, which means you’ll have access to competitive interest rates and favorable loan terms.

- What it means:

- You’ll have access to a wide range of credit products, including mortgages, car loans, and credit cards with the best interest rates.

- You may be eligible for premium credit cards that offer rewards and other benefits.

800-850: Exceptional

A score in this range is excellent! You’re seen as a model borrower, and you’ll have access to the best financial products available. Lenders are confident that you can handle credit responsibly, and as a result, you’ll likely enjoy the lowest interest rates and most favorable terms.

- What it means:

- You’ll receive the best credit offers, including ultra-low interest rates and high credit limits.

- You’re in a strong position to negotiate the terms of loans, credit cards, or mortgages.

Conclusion

Your credit score is an important piece of your financial health, but improving it doesn’t have to be overwhelming. Small, consistent actions can lead to big improvements over time. Improvements can impact all of your credit reports and scores, not just your Experian credit report and score.

With Dovly’s AI-powered credit repair, you can dispute errors, track your credit score, and take control of your financial future. Getting started is easy—sign up for Dovly today and take control of your credit journey with AI-powered insights.

Frequently Asked Questions

How do I boost my Experian credit score?

How do I get my Experian credit score higher?

How to get a 700 credit score in 30 days?

Is 700 a good score on Experian?

COMPANY

CREDIT HELP

LOCAL PAGES

COMPARE OPTIONS

© 2026 Dovly, Inc. All rights reserved.