Kikoff vs Ava: Which Is Better for Building and Improving Your Credit?

Building and improving your credit is essential for long-term financial health, impacting everything from loan approvals to interest rates and access to new credit cards. Your credit history, credit score, and payment activity all play a role in how lenders evaluate you for personal loans, car loans, mortgages, and other financial products. Platforms like Kikoff and Ava are popular credit building apps that have become popular services for users looking to boost their credit, but they serve different purposes and focus on different credit bureaus. While both offer credit-building tools, neither provides a fully proactive solution for monitoring, fixing, and improving credit over time. For consumers seeking a more complete, all-in-one credit improvement platform, Dovly AI offers a smarter alternative that goes beyond basic credit building apps.

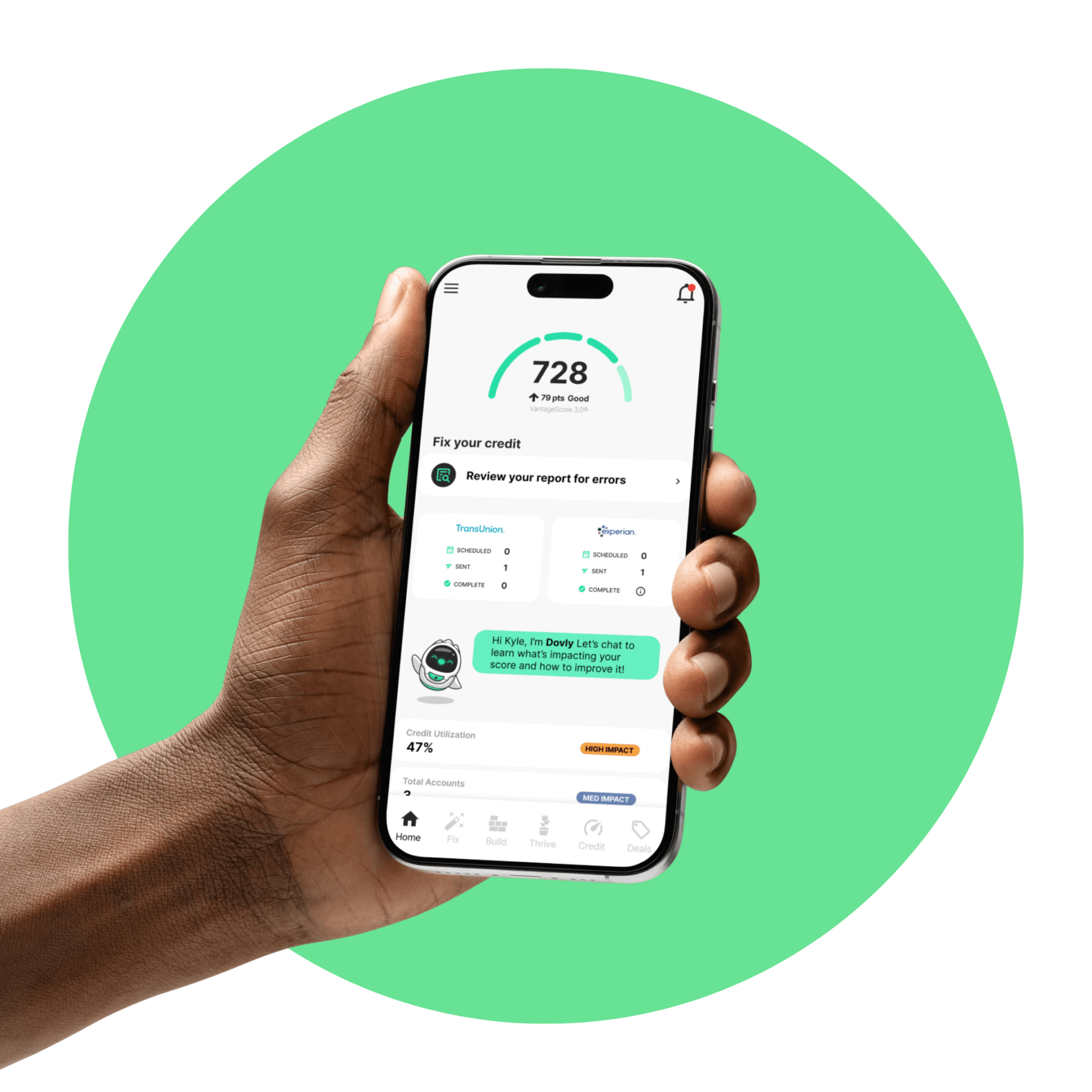

Dovly AI stands apart from traditional credit building apps by focusing on actively improving your credit and protecting your financial life. While Kikoff and Ava primarily help users build payment history through a credit builder bank account, Dovly AI works behind the scenes to identify and correct issues on your credit report that may be holding your score back. By working directly with TransUnion, Dovly AI helps users address inaccurate or outdated information through automated dispute support, creating real opportunities for score improvement.

In addition to credit monitoring, Dovly AI offers tools designed to strengthen your overall credit profile and financial services. This includes tracking account activity, monitoring payment history (including streaming services) and helping users stay aware of changes that could affect their credit utilization or credit mix. Unlike platforms that require monthly fees just to access guidance, Dovly AI provides meaningful tools for free, with a premium plan offering deeper support for users who want more.

Dovly AI also prioritizes protection alongside improvement. With fraud alerts and data breach monitoring comparable to identity theft insurance, users gain added peace of mind knowing suspicious activity tied to their bank accounts, savings account, credit cards, or other reported accounts won’t go unnoticed, helping safeguard your money. Combined with pre-qualified offers and insights designed to positively impact credit over time, Dovly AI delivers a more complete, action-oriented solution for people who want to build credit, fix errors, and move closer to their financial goals.

What You Can Achieve with Dovly AI

Get approved for credit cards

No more denials based on outdated information.

Plan for major life milestones

Don’t let credit hold you back.

Buy a house or apartment

Lenders value a strong, stable credit score.

Save thousands on interest

A better score means better rates.

Purchase a car

Secure lower interest rates and better loan terms.

Achieve financial independence

Take control of your credit and your future.

– Paisley G.

I absolutely love this app. It does everything. I am so happy to be living in the age of AI

– Brett B.

– Hannah T.

✅ Start Free with Dovly AI Today

No calls. No paperwork.No commitment.

Just your score—going up.

COMPANY

CREDIT HELP

LOCAL PAGES

COMPARE OPTIONS

© 2026 Dovly, Inc. All rights reserved.