Credit Karma vs MyFICO: Which Is Better for Monitoring and Improving Your Credit Score?

Tracking and improving your score can feel overwhelming, especially when lenders rely on different credit scoring models, bureaus, and data—such as your payments history—to make lending decisions. Your credit report, financial history, cc debt, and other credit scores all play a role in how you qualify for loans, credit cards, auto loans, and mortgages—making regular credit monitoring and identity monitoring an important part of managing your financial health.

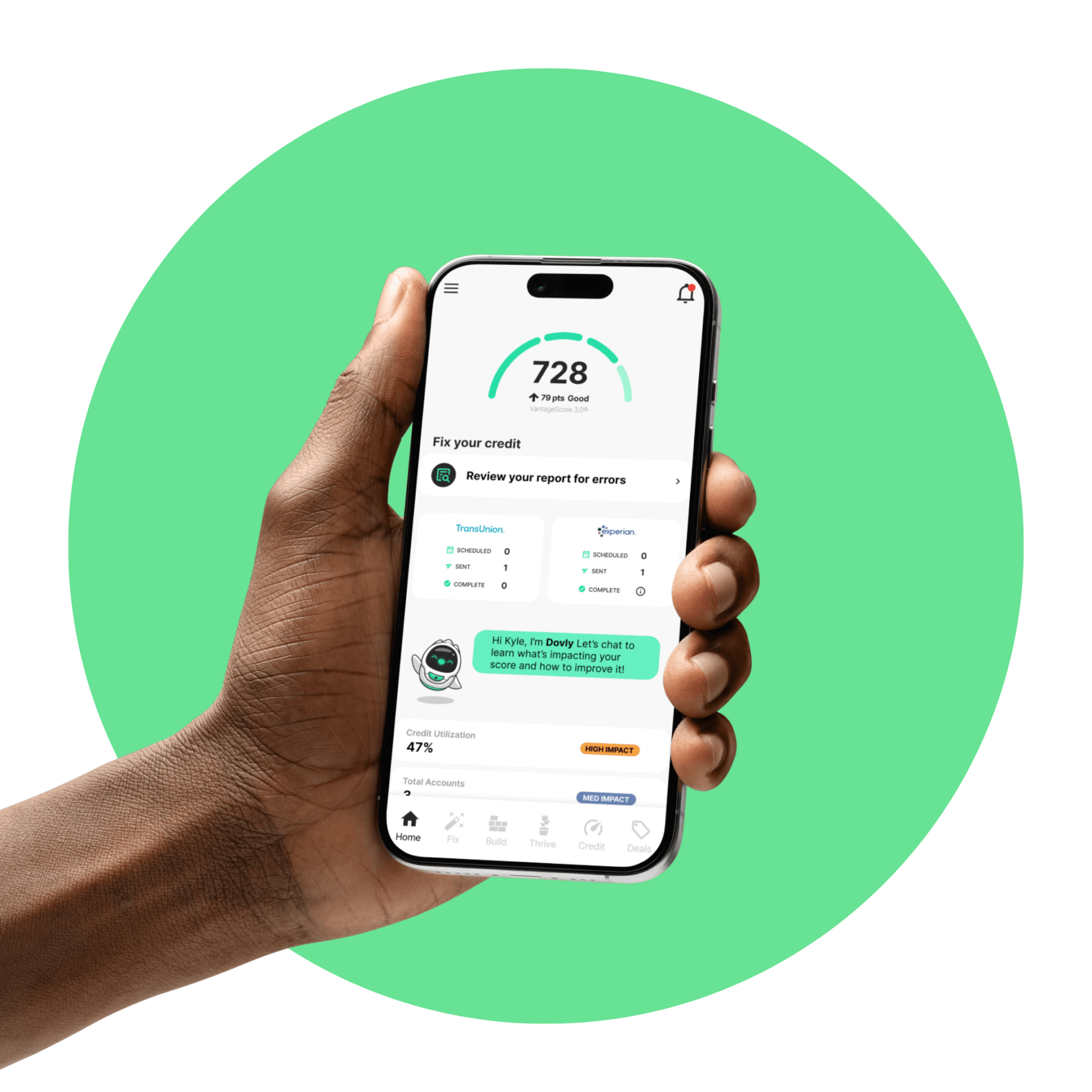

Dovly AI doesn’t just display your credit scores or reports—it actively helps improve them. Unlike Credit Karma and MyFICO, which primarily provide monitoring and updates, Dovly AI is a full credit improvement platform.

It offers no-cost credit monitoring with access to your TransUnion reports and scores, plus automated dispute support that corrects inaccuracies directly with the credit bureau—helping meaningfully improve your credit. Dovly AI also includes credit building tools to strengthen your credit history and overall financial profile, along with fraud alerts and features comparable to identity theft insurance, giving extra protection against potential threats.

What You Can Achieve with Dovly AI

Get approved for credit cards

No more denials based on outdated information.

Plan for major life milestones

Don’t let credit hold you back.

Buy a house or apartment

Lenders value a strong, stable credit score.

Save thousands on interest

A better score means better rates.

Purchase a car

Secure lower interest rates and better loan terms.

Achieve financial independence

Take control of your credit and your future.

– Paisley G.

I absolutely love this app. It does everything. I am so happy to be living in the age of AI

– Brett B.

– Hannah T.

✅ Start Free with Dovly AI Today

No calls. No paperwork.No commitment.

Just your score—going up.

COMPANY

CREDIT HELP

LOCAL PAGES

COMPARE OPTIONS

© 2026 Dovly, Inc. All rights reserved.